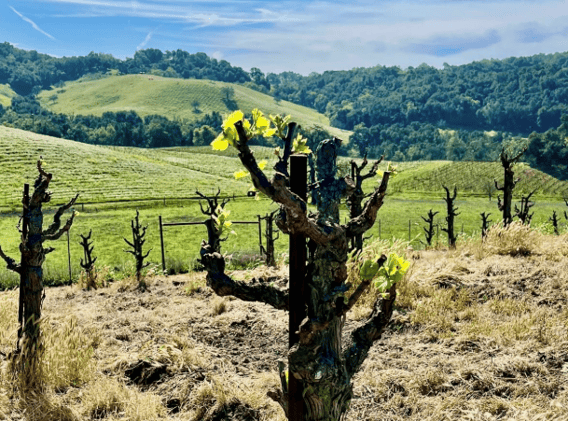

Budbreak 2026 arrives two weeks early... and this week's potential record heat means it will spread fast // Fears for the future of Argentina’s wine industry as figures hit a record low

March 17, 2026 - Wine Industry Insight Daily News Feed

2025 Grape Crush Report: Ciatti Comments // 2 Years Of Panic. Now The Wine Industry’s Survivors Are Rewriting The Rules

March 16, 2026 - Wine Industry Insight Daily News Feed

Ciatti California Report - March 2026 // Memento Mori Co-Owner Purchases Napa's Historic Edge Hill

March 13, 2026 - Wine Industry Insight Daily News Feed

Mercer Wine Estates acquires Matthews, related brands // Wine Sales Symposium Opens Registration for 2026 Event—Confronting the New Realities of Wine Sales

March 12, 2026 - Wine Industry Insight Daily News Feed

Napa County ends winery code compliance program // Goldwater Institute: Unconstitutional California Winery Mandate Must End

March 11, 2026 - Wine Industry Insight Daily News Feed

Archive