Faceblock: Meta's Unexpected Crackdown on Alcohol Content // The Reason Americans Have Stopped Drinking Out

April 6, 2026 - Daily News Feed

Who Really Pays for Tariffs? These Scholars Tracked a Bottle of Wine To Find Out // This $29 Billion Food Supply Deal Is Freaking Out Independent Restaurants

April 3, 2026 - Wine Industry Insight Daily News Feed

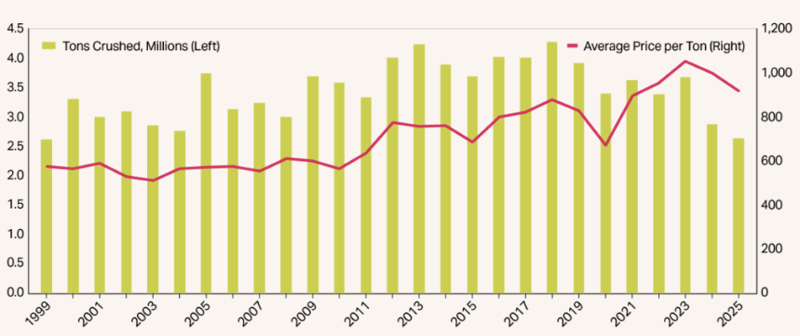

2025 Grape Crush Not as Small as Expected // Beverage alcohol suffers global downturn in 2025

April 2, 2026 - Wine Industry Insight Daily News Feed

A New York vintner raids US wine cellars to skirt Trump's tariffs // Inside the debate on wine and water use

April 1, 2026 - Wine Industry Insight Daily News Feed

Acker Makes History with Sale of World’s Most Expensive Bottle of Wine Ever Sold at Auction // National Grape Research Alliance Launches 2026 National Research and Funding Strategy

March 31, 2026 - Wine Industry Insight Daily News Feed

Archive